| Ever since the Rockefellers gave up selling snake oil to get into plain old crude oil, the petrochemical mafia has been transforming the world in its own image. From the destruction of America’s streetcar infrastructure to the countless wars of aggression in oil-rich areas around the world to the the creation of the “petrodollar” in the wake of the Bretton Woods collapse, the world’s political and economic fate over the past century has depended more on this “black gold” than most people ever imagine.

Of course it’s a scam. It always has been, ever since the first cartels formed around the drilling, transport and refining of oil. But, love it or hate it, moves in the oil markets dictate (or at least influence) geopolitical and financial events across the globe to this very day.

Today let’s delve into five recent stories from the oil markets that tell us something about the world we’re living in and where the oil-igarchs plan on taking us.

1. The Rise of the Petroyuan?

Earlier this week it was confirmed that Russia beat out Saudi Arabia as China’s number one supplier of crude oil for the second time this year. This fact may not sound significant at first glance, but to the informed eye it tells us that there are some tectonic shifts taking place both geopolitically and economically that could transform the world monetary system in the coming decades. Earlier this week it was confirmed that Russia beat out Saudi Arabia as China’s number one supplier of crude oil for the second time this year. This fact may not sound significant at first glance, but to the informed eye it tells us that there are some tectonic shifts taking place both geopolitically and economically that could transform the world monetary system in the coming decades.

Sound overblown? Well consider that China is not only the world’s number one energy consumer and number one oil importer, but it is single-handedly expected to account for 25% of the growth in global demand next year. Consider also that Russia’s investment in oil transport infrastructure (specifically the ESPO pipeline for pumping Siberian crude down to its port on the Sea of Japan) is combining with a renewed trading partnership between Moscow and Beijing that includes an agreement between Gazprom Neft and the China National Petroleum Corporation to settle all oil contracts directly in yuan. And consider also that Saudi Arabia has been the backbone of the petrodollar system since the 1970s when Kissinger convinced the House of Saud to settle all oil sales in dollars and recycle those dollars back through the US financial system through the puchase of US treasuries.

So what does this all add up to? The first signs of a potential emerging rival to the global hegemony of the US dollar that the world has seen since the dollar became the world reserve after World War II.

Now let’s be clear: the yuan isn’t about to displace the dollar anytime soon. Their markets aren’t deep enough, their currency isn’t convertible enough, their trading relationships aren’t broad enough and–perhaps most importantly–their military isn’t strong enough to back a global reserve…yet.

But the move to price their oil trades directly in renminbi is undeniably the larval stage of a move toward a de-dollarized system, as is the launch of the China International Payment System and the creation of renminbi trading hubs around the world and the Bank of China’s decision to join the LBMA gold price auction and any number of other projects embarked on in recent years.

So are we facing the rise of the petroyuan, as some | headline | writers | suggest? Not quite. But the birth of the infrastructure for what could become the petroyuan? That seems undeniable.

2. ISIS Inc.

The Rothschild Nikkei Financial Times has an unintentionally revealing series of reports this week on how ISIS is funding its jihad in Syria and Iraq through oil sales. The reports detail how the NATO/Gulf state/Turkey backed terrorists have created a “bustling trade” in oil that is now pulling in as much as $1.5 million a day.

Their secret? A surprisingly professional corporate infrastructure for overseeing the pumping, transport and sale of the oil (to their enemies and captives as much as their friends). This includes open recruitment of engineers and specialists by their “human resources department” and strict accounting measures to make sure every sale is carefully tallied and all funds are properly collected.

Oh, and it probably helps that their coalition “enemies” are leaving them alone.

That’s right. Smack dab in the middle of this mainstream report on the fearsome and incredible boogeyman du jour is an interesting infographic. It tells us that of the 10600 air strikes launched by the US-led coalition in the past 15 months, a mere 196 have bothered to target this oil infrastructure. Apparently, disrupting the enemy’s main monetary supply line just isn’t a priority for the coalition, which should only come as a shock to those who believe the coalition’s primary aim has been to actually get rid of ISIS. That’s right. Smack dab in the middle of this mainstream report on the fearsome and incredible boogeyman du jour is an interesting infographic. It tells us that of the 10600 air strikes launched by the US-led coalition in the past 15 months, a mere 196 have bothered to target this oil infrastructure. Apparently, disrupting the enemy’s main monetary supply line just isn’t a priority for the coalition, which should only come as a shock to those who believe the coalition’s primary aim has been to actually get rid of ISIS.

The new Russian/Iraqi/Syrian coalition has already called the coalition’s bluff in a number of ways. Now, if they are serious about getting rid of ISIS watch for the next wave of SU-34 and SU-24M sorties to start doing significant damage to ISIS’ (so far unmolested) oil operations.

3. Petrobras scandal

Brazil is falling off the economic cliff. This much is not in question, and perhaps not surprising to those who saw the impressive economic gains of the past decade squandered by mismanagement, waste, fraud, corruption, over-reliance on Chinese trade and a false sense of security.

But that investors are now actively warning people away from the country’s former economic crown jewel, Petrobras? That’s a turn of fortune that not many would have predicted.

The fall from grace of the once-mighty oil giant centers on the largest corruption scandal in the history of the country. After his arrest on money laundering charges last year, Paulo Roberta Costa, Petrobras’ former chief of refining, spilled the beans on a vast system of bid-rigging and bribery that assured plush oil contracts with the state-run oil giant in return for kickbacks to politicians. The scandal, unsurprisingly, is now international, with the British now up in arms over taxpayer money getting caught up in deals between UK construction firms and Petrobras.

The result? Petrobras has fallen from its position as the fourth largest energy company in the world with a market cap of over $314 billion to a minor footnote in the energy markets with a market cap of just over $30 billion, most of that loss occuring in the last year. And the company’s economic woes are far from over. An audacious sale of $2.5 billion in 100 year bonds earlier this summer earned the company some high-level enemies (including Pimco and Fidelity) after the bonds collapsed in value, and you know you’re in trouble when the Bill & Melinda Gates Foundation Trust is suing you for misrepresenting your financial situation. The result? Petrobras has fallen from its position as the fourth largest energy company in the world with a market cap of over $314 billion to a minor footnote in the energy markets with a market cap of just over $30 billion, most of that loss occuring in the last year. And the company’s economic woes are far from over. An audacious sale of $2.5 billion in 100 year bonds earlier this summer earned the company some high-level enemies (including Pimco and Fidelity) after the bonds collapsed in value, and you know you’re in trouble when the Bill & Melinda Gates Foundation Trust is suing you for misrepresenting your financial situation.

But perhaps even more important than the economic impact of the scandal is the political destabilization it has added to Brazil’s already volatile mix. The allegations of corruption went all the way to the top, with suspicion falling on President Dilma Rousseff (Energy Minister and chairman of Petrobras during much of the controversy) and her predecessor, President Luiz Inácio Lula da Silva. Although the parliamentary commission investigating the case has just cleared Rousseff and Lula of any wrongdoing, their finding that “there was no proof” of their involvement in the scandal is unlikely to instill a great deal of confidence in a Brazilian public that has already had their faith in the political system shattered.

Others were not so lucky. João Vaccari Neto, former treasurer of the country’s ruling Worker’s Party, was sentenced to 15 years for his part in accepting bribes from the company, and dozens of others have been implicated in the affair.

Although the inquiry into the scandal concluded that Petrobras was the largely innocent victim of a political cartel that was taking advantage of its position in the energy markets for their own gains, the assurances are unlikely to lure back international investors or put the Brazilian public’s minds at ease. Indeed, the latest polls show Rousseff’s approval rating plunging to 10%.

Whatever else Brazilians may be hoping for to pull them out of their economic tailspin, the oil sector isn’t likely to be the answer.

4. Trudeau to Maintain Canada’s Status Quo

Although Canadians voted overwhelmingly for Justin Trudeau’s Liberal Party in this week’s parliamentary elections in the apparent hope that they were going to be making a “clean break” with the Conservative regime of Stephen Harper, they are likely in for a rude awakening on a number of fronts.

Nowhere will this awakening be ruder than in the energy sector, where Trudeau’s left-wing activist support base is pinning their hopes on the Liberals to put various pipeline projects to rest and otherwise rein in the country’s oil and gas companies. This hope has been fostered by vague and amorphous statements by Trudeau on the campaign trail about how “addressing climate change” will be his government’s first priority on the economic agenda.

So will Trudeau really live up to his father’s reputation as an enemy of Alberta’s oil industry? Almost certainly not.

Why not? Does it have something to do with the front-and-center support of a key TransCanada pipeline consultant at Trudeau’s victory rally on Monday? Or the fact the Liberal campaign co-chair just had to resign in disgrace after emails emerged detailing how he was advising TransCanada on how best to lobby a future Liberal government?

Well, yes. But more importantly there’s no way that the Canadian economy could shake its oil dependence right now even if it wanted to. With the country having entered recession in September and the Bank of Canada still cutting its growth forecast, there is no doubt that the oil shock is already acting as a significant albatross around the economy’s neck. The BoC is even predicting a further 20% reduction in energy sector spending after a 40% drop this year. In other words, the energy sector is seizing up all by itself; no Liberal help is even needed.

But if Canadians think the oil shock is hurting their economy, they’ve got nothing on some of the more oil dependent nations…

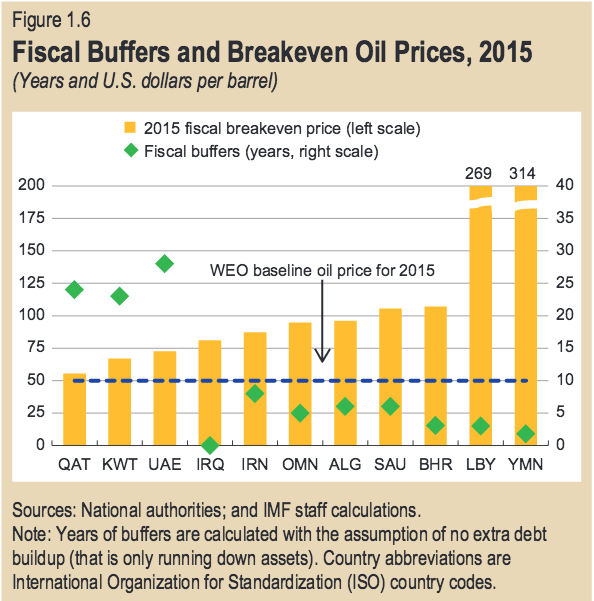

5. IMF: Gulf states are going to go bankrupt

The IMF just released their Regional Economic Outlook for the Middle East and Central Asia and there’s some bad news in there if your last name happens to be “Al Saud.” According to the Fund, Saudi Arabia, Bahrain and Oman are likely to “run out of buffers in less than five years because of large fiscal deficits” due to stagnant oil prices. As a result, the countries are going to have to massively curtail spending or start going into debt to maintain current policies. The IMF just released their Regional Economic Outlook for the Middle East and Central Asia and there’s some bad news in there if your last name happens to be “Al Saud.” According to the Fund, Saudi Arabia, Bahrain and Oman are likely to “run out of buffers in less than five years because of large fiscal deficits” due to stagnant oil prices. As a result, the countries are going to have to massively curtail spending or start going into debt to maintain current policies.

This is particularly bad news for Saudi Arabia, trying to flex its military might and wage its own illegal war of aggression in Yemen. The Kingdom has just greatly increased military spending to ramp up for a more active role in the volatile Middle East region, but now the Saudis are considering a range of cost-cutting measures to try to rein in their out of control spending.

This is all quite ironic considering the Saudis are at least partially responsible for the plunge in oil prices over the past 15 months as part of their deal with the (Long) devil John Kerry to squeeze the Russians. The move seems to have failed as Putin has doubled down on Syria and it’s the Saudis who are now in the position of blinking first and looking for the budget axe. But now that they have helped push the oil price rock down the hill they don’t have the power to get it back up by themselves. OPEC is dead (or divorced or dormant or however you want to put it) and it’s every man for himself trying to pump enough oil into an oversupplied market to make ends meet.

As we’ve discussed before, if this oil slump continues it’s going to have a profound impact on transforming economies around the globe, not just in the Middle East. Although the oil industry is responsible for much of the world’s ills over the past century, it is none the less true that millions of people have their livelihood tied directly to that industry and the economy as a whole is so closely tied in to the oil markets that this slump will result in real economic pain for many people around the globe.

But in the Saudi case that might mean having to rein in its notoriously insane extended royal family on their rape and torture binges at multi-million dollar mansions around the globe. I guess every economic cloud has a silver lining after all. |